Overview

JP Morgan Chase's Automated Customer Account Transfer (ACAT) platform is the primary way customers transfer investment assets from external institutions into Chase accounts. Since launching in August 2017, the platform processed over 2,000 account opening requests monthly—but also generated 500+ complaints in just 4 months. Leadership saw a strategic opportunity to rebuild the experience and reduce friction across all service channels.

As the deisgn lead, I served as the UX DRI and PM counterpart for discovery/prioritization, included problem framing, KPI definition, MVP scope recommendations, and Product/Engineering approved sequencing and delivery.

impact

Why This Matters

This isn't a UX flow — it's the front door for capital inflow.

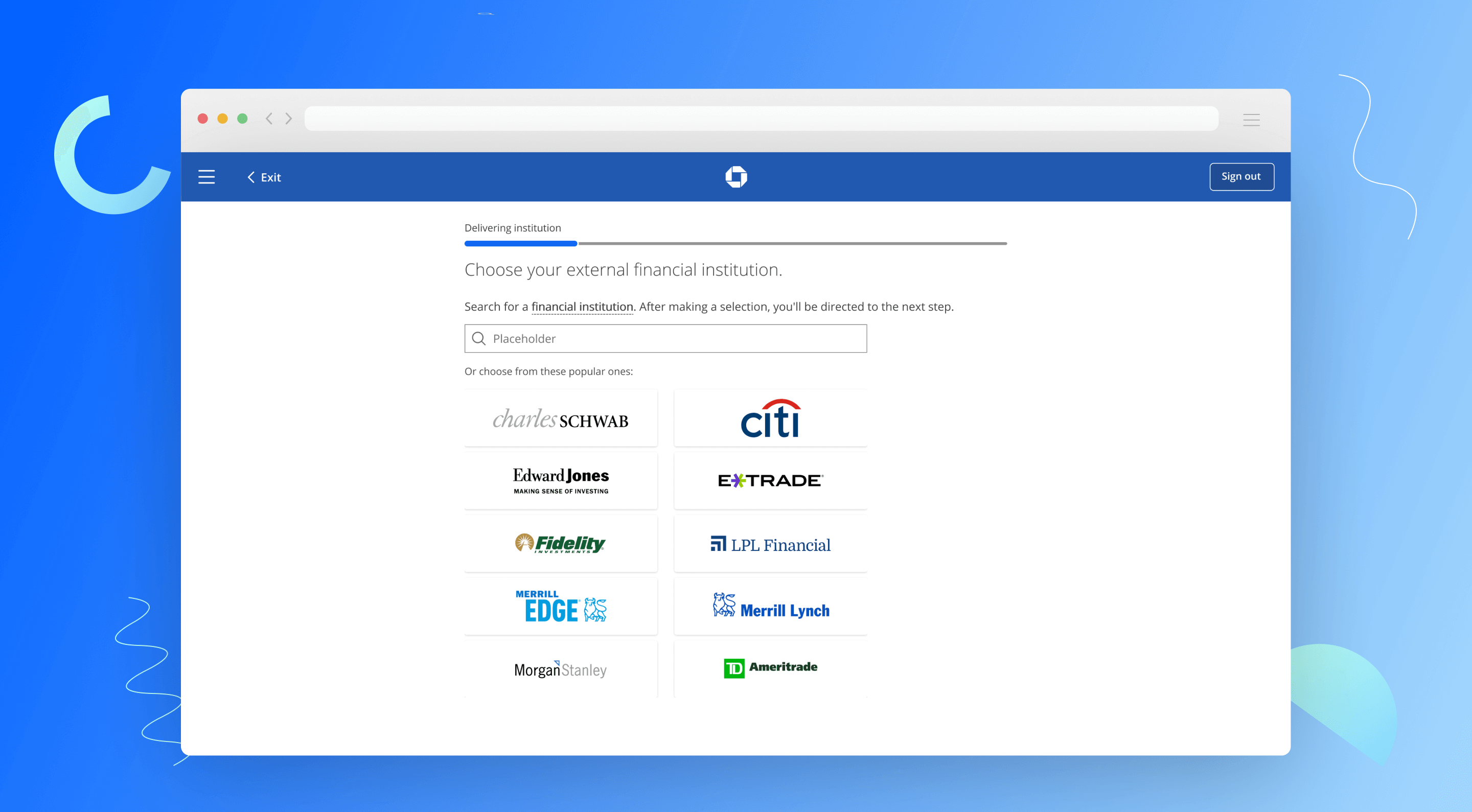

ACAT lets customers move investments from Fidelity, Schwab, etc. into Chase without paperwork or branch visits. Every friction point erodes trust and drives support cost.

Analogy: Imagine transferring money between banks, but you download a PDF, fill it by hand, mail it, then wait with no idea if it worked.

The Problem

Customers weren't stuck —they were flying blind, so they called for reassurance.

Four core issues from feedback and service data:

Baseline (call driver): The #1 reason customers called was "Where is my transfer?" — vague"pending" states with limited visibility (Call logs tagged this as the top ACAT call reason in Transfer Status).

The Strategic Bet

The real issue wasn't submission — it was uncertainty after submission.

Customers called because"pending" didn't tell them what was happening, what to do next, orwhat to expect.

Decision (receipt): I chose status transparency + expectation setting first because it addressed the #1 call driver faster than expanding institution coverage.

My Approach Before Building

I set shared success criteria first — so design decisions weren't subjective.

What I owned

- Defined KPI framework + success metrics anchored in a service blueprint

- Drove prioritization: 14 opportunities → 4 action items based on pain, feasibility,ROI

- Owned interaction model + IA for transfer tracking (status, wayfinding, recovery)

- Shipped in bi-weekly sprints across product/ops/tech

Design and launch MVP

I scoped the MVP around one goal: enough status transparency to stop the #1 call driver — not a fully-featured tracker.

When backend constraints ruled out real-time status fidelity, I made the call to ship a simplified version: confirmed submission, current stage, expected timeline. The full-vision spec stayed intact as a documented brief for the next phase. The constraint changed the vehicle, not the strategy.

What I owned: tradeoff definition, simplified tracker rationale presented to Engineering, and continuity between MVP and post-launch roadmap.

Aside from the constraints, the example below illustrates how customer frustrations were minimized with the updated online experience.

Below are a few additional finalized designs in the transfer asset journey.